Guy Dauncey is the author of Journey to the Future: A Better World is Possible and nine other books. He is an Honorary Member of the Planning Institute of BC and a Fellow of the Royal Society for the Arts.

June 2017. This is an updated and expanded version of Canada’s Housing Crisis: 22 Solutions, originally published on The Practical Utopian in December 2016.

A PDF Version of this essay can be downloaded here: Canada’s Housing Crisis – Guy Dauncey.

Executive Summary

Canada’s housing crisis is far more severe than most people realize. The fundamental problem is an excess of money pouring into the housing market from various sources, combined with an abdication of responsibility by all levels of government for the past 30 years.

There are many on-the-ground solutions, demonstrating positive ways to build affordable housing. And there are seven new housing-related taxes that could raise the funds needed for a massive expansion of affordable housing.

The fundamental cause of the problem is the excess of funds flowing into the market, and until this is solved house prices will continue to rise, and most other solutions will seem like never-ending sandbagging.

The money supply problem can be solved. The money can be obtained to restore safe, sustainable, socially designed affordable housing as a fundamental human right.

And by establishing an Affordable Housing Social Justice Connector, a permanent, hundred-year solution can be put in place that will guarantee that Canada need never confront a housing crisis again.

What is Happening?

What on Earth is happening? The explosion of housing prices in Vancouver and Victoria is crazy, but the same thing is happening in many cities around the world, not just the big ones like Toronto, London, Berlin, Paris, Stockholm, New York, San Francisco and Mumbai but also smaller communities like Kelowna, and Nashville, Tennessee. In Australia, in 2014, house prices rose by a whopping 121%.[1]

There are signs that the crisis is endemic across the developed world, which makes it likely there’s a common cause.[2] During 2015, single family house-prices in Vancouver rose by 37%. In Tsawwassen they rose by 41%; in Richmond by 36.5%. In June 2016, a very unremarkable 2,400 square foot 4-bedroom bungalow with a basement on West 29th Ave in Vancouver was on the market for $5.5 million.[3] The bubble is now beginning to slow, but by nowhere near enough to make a difference.

The housing crisis is far more serious than most people realize, and it calls for far-reaching solutions similar in scope to the way Canada’s healthcare crisis was solved in the 1960s by publicly funded universal healthcare.

Thirty years ago, if you had a reasonable income, the gap between renting and owning was bridgeable. Today, in many parts of Canada, it is not. In 1976, it took 5 years to save enough for a 20% deposit on a mortgage.[4] Today, it takes 16 years for a British Columbian to do the same—23 years in Vancouver. This poses a huge danger to the fabric of Canadian society.[5]

Over the past 15 years, the average Vancouver household’s income has grown by just 10.75%, while the cost of housing has grown by 172% (inflation adjusted). Over the same period, Toronto’s housing prices grew 188% while the median income grew by just 0.38%.[6]

A Miserable Cascade of Suffering

For here’s the thing—a third of Canadians don’t own property, and nor do their parents, so they will never inherit. Unless they win the lottery or start some genius new business they will be forced to rent for life, constantly on edge, part of the permanent minority of renters, feeding money to property owners on the other side of the divide for as long as they live.

The high rents and real estate prices are also driving young families out of the city, resulting in school closures that are disruptive for the remaining families, and tiresome commutes, cutting into the time parents have with their children. They also increase the pressures on the more vulnerable, who resort to couch surfing or living in their parents’ basements, and the super-vulnerable, who are living in the bushes and on the streets, including seniors, veterans, First Nations men and women, and families with children. It’s a miserable cascade of suffering.

Super InTent City, Victoria, Summer 2016

What does it do to a country when a third of its people are unable to own a home? Renters feel more disenfranchised. They vote less, and their needs rarely receive attention in Canada’s legislatures, where almost all politicians live on the property-owning side of the divide. On one side of the divide you borrow money to buy property. On the other, you pay rent to the property owners. The money flows one way, all the time, constantly increasing the gap between the two sides.

With fewer Canadians able to buy, the rental vacancy rates in Victoria and Vancouver are approaching zero, prompting higher rents, bidding wars by desperate families, couch-surfing, millennials living in their parents’ homes, and homelessness.[7] 40% of Canadians who rent spend more than 30% of their household income on rent and utilities, the level deemed affordable. 20% spend more than half their income, often having to choose between paying the rent and feeding the family.[8]

In Britain, where speculative sovereign wealth funds invested $26 billion in UK property in 2014, young families have been shut out of rental affordability in two-thirds of the country.[9] In America, a $15 to $25 hourly wage is needed in many states to afford a rental unit.[10] In Vancouver, you need an annual family income of $152,000 to buy a house. (2016 data)

What are the Fundamental Causes?

So what is behind it all? There are eight contributing causes:

- An excess of bank money entering the property market. Since the 1980s, and especially since 2008, there has been a far more rapid increase in the creation of money by the banks than the growth in GDP needed to absorb it. For a variety of reasons the bulk of this money is being invested in the housing market, including through popular and easy home equity lines of credit. This has been inflating the supply of money beyond the capacity of the construction industry to absorb it, resulting in property price inflation.[11

- The ability of non-Canadians to buy property in Canada with few restrictions, further inflating prices.

- The choice by Canadians with higher disposable incomes to invest their inheritances in housing, further inflating prices.

- The trend towards the commodification of housing, allowing wealthy people and investment funds to treat housing as an investment commodity.

- The failure of successive governments to invest in affordable housing, deferring to private property developers and the market.

- The failure of successive governments to address the growing crisis of poverty and income inequality.

- The failure of successive governments to end tax evasion and to regulate against property purchases for tax-evasion purposes.

- The failure of affordable housing advocates to mobilize those who are suffering from the housing crisis and help them organize themselves into a noisy, visible, political force.

In Capital in the Twenty-First Century Thomas Piketty showed why, lacking government intervention, inequality in our modern societies will continue to increase. As long as the rate of return on capital is higher than the rate of growth of the economy, he demonstrated, and unless there are policies to correct the imbalance, inherited and stored wealth will grow faster than earned wealth, constantly increasing the level of inequality.

Among the relatively well-off there are many who enjoy good salaries, generous annual bonuses and good pensions. As well as buying homes for themselves they invest some of their wealth in property, including second homes and investment properties. If ten people with similar incomes compete to buy a house, the value of the house won’t shift much. But if three can pay a lot more than the other seven, they will push the price out of reach of the seven. And if two people with identical incomes and down-payments both want to buy the same house, it will go to whoever can persuade their bank to issue the largest loan.

Two-thirds of Canadians have parents who own property, and death being what it is, sooner or later they will inherit without needing to pay inheritance taxes, paying capital gains tax only on half the value of any secondary residence. Over the next decade, CIBC reports that the boomer generation aged between 50 and 75 will inherit $750 billion, massively increasing their disposable income, much of which will flow into the property market, inflating prices.[12] As any economist will explain, if you increase the flow of money into the market for something without increasing the supply, the price will rise. Some developers argue that the solution is simply to build more housing, but with the housing crisis being a global condition, it’s a lot more complicated than that.

All this is aided by the way we allow banks to create new credit at the click of a mouse and sell the money at interest. The more they lend, the more profit they earn through the interest charged. This is a blessing, since it enables people to buy homes and build businesses, and it’s a curse, since it increases the social divide, and when it fuels a bubble it can destabilize the entire economy, leaving the public to bail out the banks, as happened in various countries in 2008.

For many years, investors have been treating housing as a speculative commodity – buy for $1 million, sell for $1.2 million in a year’s time = 20% ROI. They have been riding the wave of housing price inflation, feeding the inflation to their benefit, but to the loss of everyone who needs to rent or buy an affordable home.

Into this flooding lake of bank money we can add money from inheritances, and foreign money, which in BC is chiefly from China. China has more than a million millionaires, many of whom reportedly want to live somewhere less polluted.[13] China’s wobbly stock exchange has caused many to seek better returns overseas, and the weak Canadian dollar combined with the Chinese yuan’s devaluation has driven many to Canada, encouraged by Vancouver realtors who market specifically to them.[14] If you live in one of China’s torrid, noisy, polluted cities, Vancouver’s lyrically leafy streets must seem like paradise.

As Bill Tieleman wrote in The Tyee, the National Bank of Canada has estimated that Chinese buyers spent $12.7 billion in Vancouver in 2015, accounting for about one-third of all sales, part of an estimated US$1 trillion that left China in the last 18 months seeking safe investments.[15]

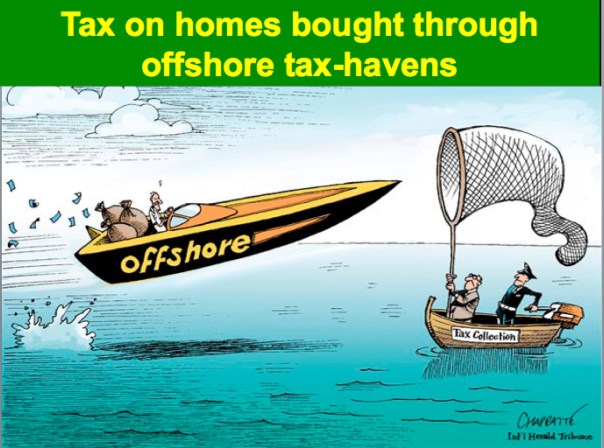

The global failure to abolish the tax havens

To the mix of suspects we must add the global failure of governments to regulate and abolish the tax havens, both offshore in places such as Barbados and the Cayman Islands, and within countries such as the US, Switzerland and Lichtenstein. This parasitic cancer on the global economy allows tax-evading millionaires to use shell companies to launder their money through property. When you enter ‘Vancouver’ in the Panama Papers search engine, Greater Vancouver lists fifteen times more addresses per population than Edmonton, indicating tax-evading shell companies where the beneficial owners are hiding their names.[16]

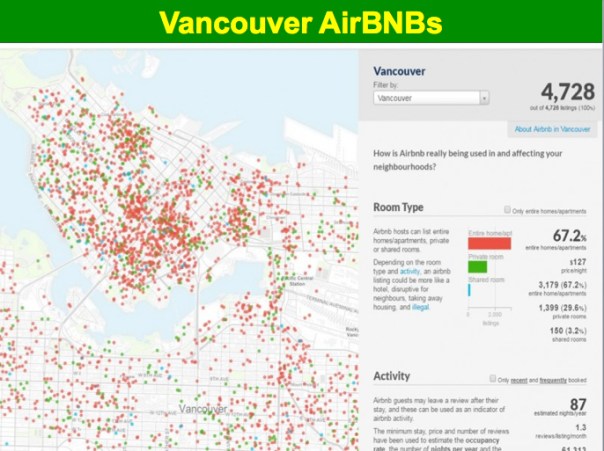

And to add grit to the wound, AirBNBs are eating into rental availability, since property-owners can generate more income from short-term rentals than from secure long-term rentals, without having to bother with the Residential Tenancy Act. In Vancouver 67% of the listed AirBNBs—3,179 units—are full apartments or houses that might otherwise be in the permanent rental pool. In Tofino, people are sleeping in the woods because rental units have been converted to AirBNBs.[17]

What Is To Be Done?

#1: Develop a Comprehensive Housing Strategy

The solutions begin with a comprehensive federal/provincial housing strategy that will end the crisis once and for all, and ensure that every Canadian has guaranteed access to a clean, safe, secure, sustainable, affordable home. We need to approach the housing crisis with the same level of ambition that Tommy Douglas approached the healthcare crisis in Saskatchewan in the 1950s—as an emergency that needs a big picture, radical solution, something that Dr. Paul Kershaw from UBC and project Generation Squeeze have been arguing.[18]

The federal and provincial governments need to tackle the root causes of the problem:

- End the excess supply of money that’s flooding into the housing market from banks, inheritances, and overseas buyers;

- Gather a large pool of new revenue to finance a major affordable housing construction program;

- Create an Affordable Housing Social Justice Connector to provide a permanent 100-year solution to the problem.

Canadians need to agree that housing is a basic Charter right. Canada has ratified the 1976 UN International Covenant on Economic, Social and Cultural Rights, which states that the parties to the covenant “recognize the right of everyone to an adequate standard of living for himself and his family, including adequate food, clothing and housing, and to the continuous improvement of living conditions,” but it has not extended this recognition as a Canadian Charter right.

The new comprehensive strategy needs to make a clean break with the failed assumption that development is best left to the market, and adopt instead the principle, clearly enunciated by UBC’s Paul Kershaw and Generation Squeeze, that “Canada’s housing market should be regulated primarily to provide an efficient supply of affordable, suitable homes for community members and families to live in (renting or owning).”[19]

The development of Canada’s National Housing Strategy is underway, following ‘Let’s Talk Housing’ feedback from many Canadians.[20]

#2. Slow the Flow of Money Into The Housing Market

Most people are unaware that banks create new money whenever they make a loan, based only on the trust that their investment will be secure. Money is not based on anything solid like gold, but on the shared belief that the promise of fair exchange that a banknote represents will be honored. Anyone can create a new currency: the problem is getting it accepted, which federal government-supported money has achieved.

Most people are also unaware that like governments in most of the western world, Canada’s government has abdicated itself from responsibility for the creation of money except for the 3% that circulates as cash, printed by the Mint at the Bank of Canada.

And most people are likewise unaware that governments have abdicated themselves of seeking to guide or control how the new money that banks create is invested. The neo-liberal economic belief is that if the economy is left to itself without government intervention, the market will find perfect equilibrium. It may be equilibrium for the economist with a secure home, but not for those whose hopes of ever owning a home have gone up in speculative smoke, who can’t afford the escalating rents, or who are living in the parents’ basement or on the street.

When the economy failed to restart after the 2008 Great Financial Crisis, central banks turned to Quantitative Easing (QE), electronically printing trillions of dollars that they gave to the banks by buying worthless and toxic securities off them, with the intention that the banks would use the money, plus the ten-to-one leverage that the new reserves would create, to lend to businesses that would create jobs. In practice, this didn’t happen. Businesses didn’t want to borrow either because they didn’t trust the market, or they were put off by the higher interest charges the banks required, and the banks ended up lending almost all of the new QE money to investors and speculators in commodities and the housing market.

From the banker’s perspective, it is easier and less risky to lend into the housing market, since a property can be sold if the buyer defaults. When they lend to a business, where the owner may have limited liability, if the business flops the owner can walk away and the bank is left holding a worthless asset. So it becomes second nature for the banks to lend into a rising-price housing market, driving prices higher, than to lend to a business.

There are three ways in which a government can re-assert control over the creation of credit:

- It can take back sovereign control over credit creation from the banks, as proposed by Positive Money in the UK, Monetative in Germany, Vollgeld in Switzerland, Sensible Money in Ireland, and the American Monetary Institute. This approach is supported by some new economists (eg Mary Mellor), and opposed by others (eg Ann Pettifor). My personal response is to oppose it. In the absence of the banks creating new money, it would need to be managed by a committee of some kind, likely composed of technocrats and economists, which Ann Pettifor suggests is the road to autocracy. The loss of day-to-day credit liquidity would also threaten enormous harm to the everyday working of the economy.[21]

- It can learn from Germany’s example, where following Article 16 of the Pfandbrief Act a mortgage cannot be offered on the current value of a property but only on its long-term permanent features under normal market conditions. This loan-to-value ratio, combined with a secure regulated rental market and a 60% value cap on mortgages has resulted in lower property valuations, lower credit requirements, and property prices that have been stable or falling since the 1970s.[22]

- It can engage in direct credit guidance, also known as ‘window guidance’, setting rules as to what proportion of new money can be invested in which sectors of the economy and suppressing unproductive credit creation. This has been widely practiced by governments in South Korea, Japan, Taiwan, and China since Deng Xiao Ping, making it difficult or impossible to obtain credit for large-scale purely speculative transactions, and it is in large part the cause of their subsequent economic success.[23]

#3. Restrict Foreign Ownership

We need to restrict the foreign purchase and ownership of land, as Martyn Brown has argued so eloquently in The Tyee.[24] We could place an outright ban on the purchase of property by foreign non-residents, as Australia and Norway have done, or do it for six months to a year while we sort our policies out, as Bill Tieleman has argued.[25] The previous BC government’s 15% additional property transfer tax on foreign buyers in Metro-Vancouver was a welcome step in this direction.

Alternatively, we could restrict the right to buy property to Canadian residents of any nationality who live and pay taxes in Canada, as Tony Greenham has argued for as a solution to Britain’s housing crisis.[26]

#4. Close the Tax Havens

Globally, Canada needs to play a far more active leadership role in the work to close down the tax havens once and for all. The economist Gabriel Zucman, in his book The Hidden Wealth of Nations: The Scourge of Tax Havens, estimates that $7.6 trillion is being hidden in the havens, including 9% of Canada’s wealth, as a result of which Canada is losing $6 billion year in government revenue. The solution he proposes is a fully transparent international finance register, backed by punitive trade tariffs against countries that refuse to cooperate.[27]

In the meantime, the federal government could require any company buying property in Canada to join a public register of beneficial ownership, showing who the actual owners are; it could impose severe punishments on professional accountants and others who enable Canadians to evade taxes; it could close the loopholes and dodgy practices that enable tax-evaders to buy and flip property in Canada; it could enable local municipalities to impose an annual tax surcharge on properties owned by offshore entities; and it could legislate the forced sale of all such properties, releasing them back onto the market.[28]

Rental Price Controls

In BC, the law limits the annual rent increase for continuously occupied residential units to 2.9%, which may be one of the best rent controls in the world. This does not apply to rental turnovers, however, which affect 30% of Metro Vancouver’s 105,000 rental units, where prices are jumping by 10-20% a year.[29]

Cities can legislate rent controls, as New York has done since 1938, and as Stockholm and Berlin are now doing to try stop rental price inflation, though their experience shows that unless the regulations are well enforced landlords will find a way to skirt the rules, and the controls can lead to a thriving black market.[30]

Adding to the muddle, developers of new rental properties need a financial incentive to build, so unduly restrictive rent controls may inhibit the very thing we need, which is more affordable rental units.

#5. Use Municipal Powers

Municipalities can use inclusionary zoning to require developers to make 30%, 50% or 100% of all new units of a development affordable and family-friendly, generating mixed-income communities.

They can zone for increased densification of single-family neighbourhoods to allow more townhouses.

They can allow car-free laneway housing and secondary suites, accompanied by good transit, safe bike-routes, and car-sharing.

They can make it easy for non-family members to buy a house together, owning it as ‘tenants in common’.

And depending on their legal powers, they can require that any new homes be marketed locally for at least six months before being offered to foreign buyers, as the Mayor of London, UK, Sadiq Khan, has proposed.

To help tackle homelessness, municipalities can also allow land left idle for more than a year to be used for temporary tiny homes villages for the homeless, learning from Dignity Village in Portland, Opportunity Village in Eugene, Oregon, and Victoria’s MicroHousing Project.[31] Cass Community Social Services, in Detroit, is successfully building a neighborhood of tiny homes for low-income residents earning as little as $10,000 a year who pay $1 a square foot, or $250 a month. Within seven years they can own their homes.

#6. A Limited Ban on AirBNBs

Vancouver is proposing to license short-term AirBNB rentals within principal residences, but to deny licenses to AirBNBs that are in separate apartments or houses, potentially releasing up to 3,000 units of housing into the permanent rental pool. The ban could be linked to the rental vacancy rate, ending when it rises above 3.0.

How Much New Housing Is Needed?

Following the 2015 Canadian federal election, anti-poverty advocates and housing providers asked the government for $3.2 billion to renovate old units and to build 100,000 new units nationwide.[32] The federal government responded with a $2.3 billion short-term commitment over two years for a variety of affordable housing initiatives.

The cost of the failure to address homelessness is estimated at $7 billion a year, because as a society we are using law enforcement, courts and prisons, emergency healthcare, longer hospital stays and emergency shelters instead of taking a proactive Housing First approach, as cities like Medicine Hat, Alberta, have done.[33] This is the cost of allowing social entropy to blossom, instead of taking a pro-active syntropic approach.

Citizens for Public Justice says 3.2 million Canadians need improved housing, because they pay more than they can afford on rent, or live in homes that are overcrowded or need major repairs.[34]

This includes Canada’s First Nations, for whom the Assembly of First Nations has estimated the on-reserve housing shortage to be approximately 85,000 units. Aboriginal Affairs and Northern Development Canada puts the number at 35,000 to 40,000 units.[35]

Seabird Island Sustainable First Nations Housing, BC

In Metro-Vancouver, 145,000 households spend more than 30% of their income on housing. Marc Lee, chief economist with the Canadian Centre for Policy Alternatives, sees the need to build 5,000 to 10,000 new units a year in Metro Vancouver alone.[36] For BC as a whole there is probably need to build 10,000 to 20,000 units of new affordable housing a year.

Such a massive building program would generate up to 22,600 new jobs for builders and the trades in BC, assuming 1.13 jobs per apartment unit.[37] It would also create an opportunity for solutions the climate crisis and the growing problem of loneliness. (See below.)

What Will It Cost?

10,000 to 20,000 units a year at $250,000 per unit comes to $2.5 to $5 billion a year, less if governments contribute land (as Vancouver is offering to do) and waive the development fees. This could finance an ambitious affordable housing building program, led by non-profits. If the new revenue comes from targeted housing taxes (see below), this would also help to cool the market. If the development is done through housing cooperatives (see below), the cost could be considerably lower.

In the pot so far is the federal government’s $2.3 billion Affordable Housing Initiative over two years, which includes $500 million for affordable housing units and various other needs, $739 million for First Nations housing, $208 million over five years for an Affordable Rental Housing Innovation Fund to support the construction of up to 4,000 affordable rental units, and $500 million for an Affordable Rental Housing Financing Initiative to provide low-cost loans to municipalities and housing developers to construct affordable rental housing.[38]

If the federal money is shared among the provinces by population, BC’s share comes to $150 million a year. In February 2016 the provincial government announced $365 million in matching funds to build 2,000 units, and in September it added $500 million to build a further 2,900 rental units. Taken together, the BC commitments come to $1 billion, providing the funds for 5,000 units, and 20-40% of the finance needed to build the 10,000 to 20,000 new affordable rental units that are needed every year to provide a permanent solution to the crisis.

Canada’s mayors are seeking $12.6 billion over ten years as part of the government’s $20 billion social infrastructure investment, including $7.7 billion to maintain and repair existing units and $4.2 billion to build 10,000 units of housing annually across the country. This comes to $1.26 billion a year for the whole of Canada, which is insufficient to solve the problem.

To accumulate the funds needed, seven sources of new revenue are needed—three municipal, two provincial and two federal (see below).

What Did BC’s Political Parties Offer?

In the May 2017 provincial election:

- The Liberals promised to build 5,300 units of affordable housing a year.

- The Green Party promised to build 4,000 units of affordable housing a year.

- The NDP promised to build 114,000 units of affordable housing over ten years, or 11,400 units a year.[39]

#7. Housing Cooperatives

If the new affordable housing was organized as housing cooperatives, backed by supportive policies, the finance might be able to come largely from the market. In Sweden, some 13,000 housing cooperatives own 998,000 dwellings, providing housing for 1.6 million people, 22% of Sweden’s population. “The tenant-owners finance 75 – 80% of the development cost and the rest of the financing is raised by the co-op organizations through loans from the banks and other private financial institutions. Tenant-owners can normally get a loan from the banks equivalent to 85% of the down-payment required.”[40] If zero-interest capital loans were advanced to cooperatives (see below), this would further reduce the cost.

Since 1976, the collaborative non-profit Batir Son Quartier in Montreal has developed 10,900 units of affordable housing, half of which are in cooperatives.[41]

Zurich, Switzerland, has no housing crisis, and it’s chiefly because the city responded long ago to its then housing crisis by offering interest-free loans to buy land for the development of cooperative housing. Today, a quarter of the city’s housing is not-for-profit, 80% of which is provided by private housing co-operatives.[42]

Affordable housing experience in Lewisham, London, UK, shows that it is important to include the future owners of an affordable housing initiative in co-designing the plans. “Involving residents directly in the process is also one way of making housing more affordable, and it does help to create a committed, localised and engaged community.”[43]

#8. Zero-Interest Capital Loans

The money does not all need come from new sources of revenue, since housing produces rent, enabling the private sector to get involved. The federal government has committed $500 million to this end, and the provincial government, which can borrow at 1%, could use the federal money to offer zero-interest capital loans to developers who build 50% or 100% rental buildings, and to housing coops.[44] The BC government lends at 1% for the property tax deferral program for seniors.

Affordable Housing Bonds, in use in Britain for 30 years, are also possible.[45] So is the development of public banking, which has proven its ability to provide stable, successful banking in North Dakota for almost 100 years.[46]

#9. An Affordable Housing Tax Levy

A municipality can enact an affordable housing tax levy. Seattle has done this since 1981, enabling the city to build 12,500 affordable apartments, help 800 families to purchase their first home, and provide emergency rent assistance to 6,500 families. The levy increases property taxes by $122 a year on a home with an assessed value of $480,000, with an exemption for homeowners whose annual income is less than $40,000, and for those who are over 60, disabled and unable to work, or veterans with service-related disabilities.[47]

#10. A Municipal Levy on Properties Bought by Non-Residents

There could be an additional municipal levy on properties bought through offshore companies, and by non-residents or non-Canadian tax-payers, at least until purchase by non-residents is restricted or ended, as UBC economist Joshua Gottleib has proposed. [48]

#11. A Municipal Levy on Empty Houses or Second Homes

Vancouver has 10,000 empty condos, while 1,750 people are homeless (3,700 in Metro Vancouver).[49] Victoria has a further 1400 homeless people. London (UK) has 50,000 empty properties and 6,500 homeless. There’s something deeply wrong with this picture. Across Canada, up to 35,000 people live in shelters or on the streets.[50]

According to Vancouver City Hall staff, if 20% of Vancouver’s empty homes were used for rentals, it would increase the rental vacancy rate from the current extremely low level of 0.6% to a healthy 3%.

Vancouver’s new annual 1% property value tax on empty properties, supported by 80% of Vancouver’s people, will cost the owner of an empty $1 million home $10,000 a year to keep it empty.[51]

Lovely view, but no-one at home to see it

#12. An Escalating Property Transfer Tax on High-End Properties

Provincially, there could be an escalating property transfer tax on high-end properties, which would also help to cool the market. In February 2016 the BC government raised the tax to 3% for the portion above $2 million, and it could go higher.

As a result of the overheated property market, the BC government has been making an unexpected killing from the property transfer tax: $1.49 billion in the last fiscal year, a 40% increase over the year before, and $562 million more than the government budgeted for. Given the damage that housing price inflation is causing, it is appropriate that 80% of the increase be earmarked for affordable housing.

#13. A Housing Speculation Tax

There could be a 10% speculation tax on properties that are bought and flipped quickly. Other changes are needed to close various loopholes that are corrupting the real estate industry, enabling some people to avoid paying property transfer tax altogether.[52]

#14. Penalties on People Who Avoid Capital Gains Tax

There could be financial penalties on people who avoid capital gains tax by falsely claiming an investment home as their primary residence, with 100% of the revenue (less costs) going into the Affordable Housing Fund.

#15. A Federal Inheritance Tax

Finally, there could be an escalating federal inheritance tax on inheritances over $1 million, with 100% of the revenue being used to build affordable housing to offset the way inheritances fuel housing price inflation. This would also help address the deeper trend of growing inequality, although much more will be needed to reverse it, including a $15 minimum wage, the end of student debt, affordable childcare and major tax reforms.

#16. Use Central Bank Quantitative Easing to Invest in Housing

As explained above, private banks and credit unions create new money every day with few or no restrictions, limited solely by their perceptions of trust and risk. Central banks can also create new money, based on trust in the country and its economy as a whole. This ability to create money “out of thin air” is an essential tool in the arsenal of financial stability, making it possible for central banks to prop up failing banks and to inject money into an economy at a time of sluggish growth. Since 2008 the world’s central banks have created and pumped some $14 trillion into economies in their attempts to stimulate growth, but most of the money has gone into the speculative housing and commodities markets, inflating prices and causing the very crisis we seek to address.

In 2015 nineteen economists including Steve Keen, David Graeber, Ann Pettifor, Robert Skidelsky and Guy Standing signed a letter to the Financial Times calling on the European Central Bank to adopt a more direct approach to its quantitative easing plan. The simple truth is that if it chooses to, or is directed to do so by its government, a central bank can stimulate the economy by the direct creation of money to build affordable housing. The government would create Affordable Housing Bonds and give them to local governments, non-profit housing associations and housing cooperatives, and the central bank would then buy the bonds, distributing the money. In the UK, this is known as Green Infrastructure QE, or QE for People.[53]

The Bank of Canada is a public bank, owned by the people of Canada, so there is no inherent obstacle to the government making a request that it issue QE money for affordable housing in this manner.

A common concern that is raised when the central banks’ ability to create money is discussed is that the increase in the money supply will cause inflation, as happened in the past whenever governments printed money to pay for their wars. In reality, to the extent that money-creation by private banks for speculative purposes is pinned back, there is room for central bank money-creation. It is also arguable that as long as inflation is kept under (eg) 3%, it is a small price to pay for ending the suffering and stress of millions of Canadians by solving the affordable housing crisis.

#17. Establish a Permanent Affordable Housing Social Justice Connector

- With the need having been established,

- the right to affordable housing having a strong case to become a fundamental human right in Canada’s Charter of Rights and Freedoms,

- the practicalities to build what’s needed being quite straightforward,

- and the sources of finance being available through new taxes and the Bank of Canada’s use of quantitative easing,

it becomes possible to sew all this together into a permanent 100-year solution.

First, an Affordable Housing Index needs to be created to measure and quantify the level of the housing crisis. A score of 100 would tell us that in any one region everyone was securely housed in affordable, warm, mould-free conditions, and not paying more than 32% of their income as rent or mortgage. A score of anything less would tell us that Canadians were still suffering housing difficulties and distress.

The Index would be calculated annually and regionally based on known data, including an identifiable data for First Nations, and be used to determine the appropriate level of taxes and federal QE needed to get the score up to 100.

An Affordable Housing Social Justice Connector would then be established to produce the volume of money needed through taxation and QE to raise the Index to 100. When the Index reaches 100, the Connector would remain in place without triggering any flow of money. Whenever and wherever the Index falls below 100, however, the Connector would channel the money needed to rectify the score. In this manner, a permanent 100-year solution can be achieved.

Working Together

With a dependable stream of new revenue, governments could work together to finance the building of 10,000-20,000 units of new affordable housing in BC, in partnership with non-profits and agencies such as the Vancouver Affordable Housing Agency.

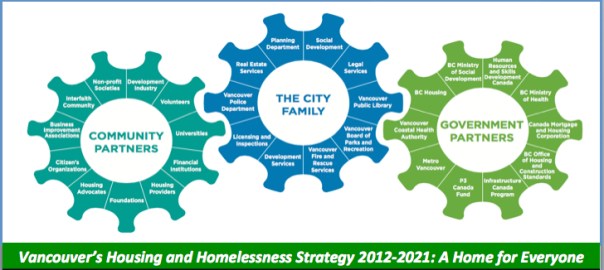

While provincial and federal governments have been asleep on the housing file for three decades, the City of Vancouver has not. It established The Mayor’s Task Force on Housing Affordability in 2011, which came up with Vancouver’s Housing and Homelessness Strategy 2012-2021: A Home for Everyone. In 2014 it established the Vancouver Affordable Housing Agency,[54] which committed 20 parcels of land for low-cost housing, and in May 2016 it announced the construction of 358 affordable housing units on four city sites. Victoria has also been very active in seeking solutions and enabling new rental developments.

#18. An Affordable Housing Land Reserve

Land being purchased for affordable housing can be placed in an Affordable Housing Land Reserve, operating as a Community Land Trust, through which the land would be taken off the market forever, but the homes could still be bought and sold for residential purposes. This would guarantee future affordability for generations to come, while allowing families to own the homes they live in and to leave them to their children in their wills.[55] This is the way Vancouver is proceeding in partnership with the Vancouver Community Land Trust Foundation.[56]

BC established a Housing Priority Initiatives Fund in July 2016, so the foundation is in place; it now needs to receive a lot more money, and focus its expenditures on land purchases placed in Community Land Trusts to support the development of new housing cooperatives.

#19. Housing First

The new stream of revenue could also enable every municipality in Canada to adopt the ‘Housing First’ approach to homelessness, giving priority to ensuring that everyone has a home to live in before focusing on mental illness, drug and alcohol addictions. Since starting on its strategy in 2009, Medicine Hat, Alberta, a city of 60,000, has eliminated 100% of its homelessness, providing secure homes in supportive or subsidized housing for 875 people, including 280 children.[57] The Canadian Alliance to End Homelessness’s 20,000 Homes Campaign is leading the charge to implement Housing First across the country, calling for 20,000 new homes to be created for the homeless by July 2018.[58]

#20. Creativity in Providing Affordable Housing

The argument for enabling non-profit housing societies to manage the building program is that they have a better understanding of the variety of housing options that are needed, they operate without a profit expectation, and they enjoy the public’s trust.

In addition to traditional building, new approaches include rent-to-own, temporary pre-fabricated modular homes, shipping container homes, and the Montreal ‘Grow-Home’ three-story townhouse, where first-time buyers start with a simple small unit, designed for expansion as a family and its income grows.[59]

Montreal’s Grow-Homes

In Holland, the government has been encouraging self-building, by which new homes, often in large-scale developments, are financed and customized by private individuals, not developers, some with help from government stimulus schemes for families earning less than $29,000 a year. Self-build now accounts for a third of all homes purchased, by-passing the financial cut that developers expect to make.[60]

Holland’s Self-Build Affordable Housing

Another model is the Whistler Housing Authority, established in 1997 to address the chronic shortage of staff housing in the resort. Through their work, more than 1,000 properties are available only to local employees and retirees. If you want to buy one of the units, and wish to sell, the price increase is limited to the rise in Canada’s national price index, not the local property market, enabling Whistler to keeps its units affordable in perpetuity.[61] Vancouver’s new Affordable Home Ownership Pilot Program works on similar principles, with at least one person needing to be a first-time buyer who works in the city.[62]

#21. Student Housing

For student housing, where there is an urgent need for 20,000 new units in BC, the universities have said that they are ready and willing to self-finance their own projects. All that is needed is a provincial arrangement that the debt would not fall within the government’s total capital debt, which affects the province’s credit rating. At an estimated $100,000 per unit, this is the most cost-effective way to relieve rental pressures in Victoria, Vancouver and Burnaby.

#22. Passive Homes

To tackle the climate crisis we need—among other things—to eliminate the use of fossil fuels, in part by using 100% renewable energy in new buildings. Passive Houses reduce heat-loss by 90%, thanks to their extra-thick insulated walls and triple-glazed windows, and they need no heat-source apart from a small electric heat-recovery ventilator. They are zero-emission homes.[63]

Based on experience in Victoria, where Rob and Mark Bernhardt are building Passive Homes, they cost only 4.4% more.[64] With no heating bill, the small extra cost can be easily absorbed into the financing. In Brussels, Belgium, since 2015, every new building, large or small, has been required to be built to the Passive House standard.[65] If BC was to build 10,000 to 20,000 sustainable, affordable Passive Homes a year, it would catapult us into world leadership and create a wave of similar change around the world.

Passive House Condos in Victoria, BC

#23. Sociable Homes

It is also important to design the layout of new homes to make them sociable, to address the growing problem of loneliness. The human instinct to connect is very strong, and when allowed to blossom it builds communities where people take care of each other. When suppressed, however, due to thoughtless design, people become isolated, leading to loneliness, which accentuates stress and mental illness.

For 99.99% of the last million years our ancestors lived together in communities, doing everything on foot. It was only 70 years ago, in the 1940s, that planners declared automobile access to be more important than human contact, restricting humans to sidewalks, and giving approval to suburbs that often have no sidewalks at all and no places where neighbors can meet and socialize.

It is important, therefore, that as well as being built to the Passive House standard, and including green space, allotment gardens and play space, every new affordable housing project be designed to be sociable, using a participatory design process and shared leadership, with natural meeting places, and car access off to one side, like the much sought-after UBC student family housing at Acadia Park,[66] and the pocket neighborhoods that the architect Ross Chapin has designed on Whidbey Island in Washington State.[67] When local considerations require that there must be car-access among the buildings, and not off to one side, the road can be based on the Dutch principle of woonerf or ‘living street’, where humans have priority and cars no longer have the automatic right of way.

A Pocket Neighbourhood

#24. New Villages

A growing number of people want more than an affordable home. They want to live in an ecologically sustainable community where they can share, grow food and develop projects together.

They also want to enjoy a stronger sense of community. They want to build a sharing economy with a lighter footprint on the Earth. They want to build tiny home villages and ecovillages.

Tiny home village living in converted whisky-barrels. Findhorn Ecovillage, Scotland

To turn these desires into reality requires a willingness to train people in the skills of land development, financing and zoning. In Canada’s early history many people went out and built their own towns and villages without much difficulty. These days, however, the complexity of land development, finance, investors, planning, zoning, development permit applications and water, sewage and roads approvals means that almost all development is done by developers working by professional planners, surveyors and engineers.

The history of cohousing, however, with ten completed projects in in BC, shows that land development can be managed democratically by the residents themselves, using professional help where needed.[68] It is possible to imagine a platform being created that would assist people to create tiny home villages and ecovillages.

We could use a small portion of the affordable housing funds to train people how to become their own developers, forming Ecovillage Development Cooperatives, raising the finance, and navigating the complex world of zoning and development approval.

Roberts Creek Cohousing, Sunshine Coast, BC

Conclusion

Using these solutions, we could turn the housing crisis into a great opportunity to build affordable homes that also build community and contribute a solution to the climate crisis.

Could it happen? It could if enough municipal councils, non-profits, businesses and service clubs get behind it, urging our provincial and federal politicians to embrace solutions such as these, and show leadership.

#25. A Canadian Affordable Housing Alliance

It could also happen if a broadly-based Affordable Housing Alliance was established through which not just the leading NGOs but the millions of Canadians who struggle to buy a home or pay the rent could organize, the way agricultural workers did when they formed the first labour unions in the 1800s.

It was only after Victoria’s Super InTent City made so many headlines, ruffled so many feathers and won its court cases in the summer of 2016, assisted by Victoria’s Together Against Poverty Society and many others, that the city and the province came together to find $86 million to finance 714 new housing units for homeless people. Some people complained that the Super InTent City’s leadership was activist, but that is exactly what is needed, not just in Victoria but every community.[69]

One thing is certain: without deep, intentional solutions this crisis will only get worse. More millennials will be shut out of home ownership, more people will experience the stress of unaffordability in the rental market, more people will be obliged to couch-surf or to remain living with their parents, more people will live in vans and trucks, more people will become homeless, and more angry Tent Cities will spring up—and not all will be as well organized as Victoria’s was.

*

July 6, 2017 Addition

Solution #26

In July 2017, in The Tyee, Tex Enemark wrote about significant changes to the way the construction properties are taxed that were implemented in 1972, which caused many developers to cease building rental properties. Reversing the changes, he argues would restore the incentives to built:

- Treat rentals the same as motels, hotels and family farms

- Restore “rollover” provisions and GST exemptions

- Allow qualifying rental owners to claim the small business tax rate and “active business” tax treatment.

- Restore the Capital Cost Allowance to 1972 levels and allow investors and owners to write off losses against non-rental income.

Guy Dauncey is the author of Journey to the Future: A Better World is Possible, and nine other books. He is an Honorary Member of the Planning Institute of BC, a Fellow of the Findhorn Foundation in Scotland, and a Fellow of the Royal Society for the Arts. See www.journeytothefuture.ca

End-Notes

[1] Will housing bubble pop in 2017? ABC News May 22, 2015. www.news.com.au/finance/real-estate/buying/will-housing-bubble-pop-in-2017/news-story/4fe05fed1c277a096df33242a26caf6c

[2] Damning report exposes Europe’s escalating housing crisis. Guardian, Nov 19, 2015. www.theguardian.com/world/2015/nov/19/damning-report-exposes-europes-escalating-housing-crisis

[3] 3538 West 29th Ave, Vancouver: www.rew.ca/properties/R2072511/3538-w-29th-avenue-vancouver

[4] Code Red: Rethinking Canadian Housing Policy. Dr. Paul Kershaw and Anita Minh. Generation Squeeze, Spring 2016. www.gensqueeze.ca/code_red_rethinking_canadian_housing_policy

[5] Mayor Gregor Robertson warns that unsustainable increases in housing prices threaten Vancouver economy. Georgia Strait, June 5, 2015. www.straight.com/news/711671/mayor-gregor-robertson-warns-unsustainable-increases-housing-prices-threaten-vancouver

[6] It’s Not Just You: Vancouver Housing Up 172%, Income Just 10%. Better Dwelling, June 30, 2016. https://betterdwelling.com/city/vancouver/its-not-just-you-vancouver-housing-up-172-income-just-10/

[7] Affordable housing crisis forcing some Okanagan families onto the streets. CBC News, June 8, 2016. www.cbc.ca/news/canada/british-columbia/affordable-housing-crisis-forcing-some-okanagan-families-onto-the-streets-1.3621221

[8] Affordable housing crisis affects one in five renters in Canada: study. Globe & Mail, Sept 10, 2015. www.theglobeandmail.com/real-estate/the-market/affordable-housing-crisis-affects-one-in-five-renters-in-canada-study/article26287843/

‘I Go to Bed in Tears’: Lower Mainland Renter Rage. Dermot Travis, The Tyee, June 16, 2016. http://thetyee.ca/Opinion/2016/06/17/Lower-Mainland-Renters-Rage/

[9] Young families priced out of rental markets in two-thirds of the UK. Guardian, March 14, 2016. www.theguardian.com/world/2016/mar/14/young-families-priced-out-rental-markets-in-two-thirds-uk

[10] Mapping the Hourly Wage Needed to Rent a 2-Bedroom Apartment in Every U.S. State. CityLab, May 25, 2015. www.citylab.com/housing/2015/05/mapping-the-hourly-wage-needed-to-rent-a-2-bedroom-apartment-in-every-us-state/394142/

[11] Why consumers should be wary of using the wildly popular home equity lines of credit as ATMs. Financial Post, June 7, 2017. http://business.financialpost.com/personal-finance/home-equity-lines-of-credit-may-lead-canadians-to-use-their-home-as-atms-consumer-agency-warns

[12] Baby Boomers To Inherit $750 Billion In Largest-Ever Canadian Transfer Of Wealth. Huffington Post, June6, 2016. www.huffingtonpost.ca/2016/06/06/cibc-canada-in-line-for-a-bequest-boom-as-750-billion-of-assets-passed-on_n_10318872.html

Vancouver condo marketer Bob Rennie doubts city’s affordability plan. Globe & Mail, June 2, 2016. www.theglobeandmail.com/news/british-columbia/vancouver-condo-marketer-bob-rennie-doubts-citys-affordability-plan/article30256305/

[13] China has more than 1 million millionaires. CNN Money, May 25, 2015. http://money.cnn.com/2015/05/27/luxury/china-million-millionaires/

[14] Ian Young on Vancouver’s ‘freakshow’ housing market. MacLean’s, May 10, 2016. www.macleans.ca/economy/economicanalysis/ian-young-on-vancouvers-freak-show-housing-market

[15] ‘China Syndrome’ Paralyzes Politicians in Housing Affordability Crisis. Bill Tieleman, The Tyee, June 21, 2016. http://thetyee.ca/Opinion/2016/06/21/China-Syndrome-Housing-Paralyzes-Politicians/

[16] Panama Papers database includes hundreds of Metro Vancouver addresses linked to offshore accounts. Georgia Strait, May 9, 2016. www.straight.com/news/694676/panama-papers-database-includes-hundreds-metro-vancouver-addresses-linked-offshore

Panama Papers: Vancouver is Canada’s hotspot for secret tax haven firms, with hundreds of addresses in leaked papers. South china Morning Post, May 25, 2016. www.scmp.com/news/world/united-states-canada/article/1953614/panama-papers-vancouver-canadas-hotspot-secret-tax

[17] AirBNB wreaks havoc on Vancouver rental scene. Vancouver Courier, March 9, 2016. www.vancourier.com/opinion/airbnb-wreaks-havoc-on-vancouver-rental-scene-1.2194418

[18] Generation Squeeze: www.gensqueeze.ca

[19] Generation Squeeze: www.gensqueeze.ca/homes_first

[20] See www.letstalkhousing.ca

[21] For an overview, see Sovereign Money: www.sovereignmoney.eu. For a critique, see Pettifor, Ann. The Production of Money – How to Break the Power of the Bankers. Verso, 2017.

[22] How Germany achieved stable and affordable housing. Macrobusiness, June 22, 2011. https://www.macrobusiness.com.au/2011/06/how-germany-achieved-stable-affordable-housing/

[23] See Where Does Money Come From? A Guide to the UK Monetary and Banking System, by John Ryan-Collins, Tony Greenham, Richard Werner and Andrew Jackson. Chapter 5. New Economics Foundation, 2011.

[24] Martyn Brown: An essay on B.C.’s housing crisis and what to do about it. Georgia Strait, May 19, 2016. www.straight.com/news/702206/martyn-brown-essay-bcs-housing-crisis-and-what-do-about-it

[25] My fix for the housing crisis: ban ownership by foreign non-residents. Zoe Williams. Guardian, May 22, 2015. www.theguardian.com/commentisfree/2015/jun/22/housing-crisis-ban-ownership-foreign-non-residents

Stop rich overseas investors from buying up UK homes, report urges. Guardian, Feb 1, 2014. https://www.theguardian.com/business/2014/feb/01/rich-overseas-investors-uk-eu-housing-market

Serious About Housing Costs? Ban Foreign Home Sales for Six Months. Bill Tieleman, The Tyee, June 14, 2016. http://thetyee.ca/Opinion/2016/06/14/Vancouver-Foreign-Ownership-Sales-Ban/

[26] Why only UK Taxpayers should own UK homes. Tony Greenham, RSA. April 7, 2016. www.thersa.org/discover/publications-and-articles/rsa-blogs/2016/04/no-domicile-no-domus-why-only-uk-taxpayers-should-own-uk-homes

[27] The Hidden Wealth of Nations: The Scourge of Tax Havens, by Gabriel Zucman. Chicago University Press, 2015. www.amazon.ca/Hidden-Wealth-Nations-Scourge-Havens/dp/022624542X

[28] Out of the shadows: Kathy Tomlinson reveals how loopholes and lax oversight are making it easy for a network of local and foreign speculators to play the system, and, in the process, fuel the steep rise in Vancouver home prices. Globe & Mail, Sept 13, 2016. www.theglobeandmail.com/real-estate/vancouver/out-of-the-shadows/article31802994/

[29] Barbara Yaffe: Vancouver rent increase ‘tsunami’ expected. Vancouver Sun, July 26, 2015. www.vancouversun.com/business/Barbara+Yaffe+Vancouver+rent+increase+tsunami+expected/11246784/story.html

[30] Berlin’s New Rent-Control Law Probably Isn’t Working After All. CityLab, Feb 1, 2016. www.citylab.com/housing/2016/02/berlin-rent-control-cbre-report/458700/

New York’s rent controls: ‘essential for the future of the city‘. Guardian, Aug 19, 2015. www.theguardian.com/us-news/2015/aug/19/new-york-rent-controlled-homes

Pitfalls of rent restraints: why Stockholm’s model has failed many. Guardian, Aug 19, 2015. www.theguardian.com/world/2015/aug/19/why-stockholm-housing-rules-rent-control-flat

Would a rent cap work for tenants facing £1,000-a-month rises? Guardian, May 2, 2016. www.theguardian.com/money/2016/may/02/would-rent-cap-work-tenants-1000-a-month-rises

[31] Home Petite Home. BuzzFeed, Jan 15, 2015. www.buzzfeed.com/timmurphywriter/tiny-homes

Victoria MicroHousing: www.microhousingvictoria.com

[32] Canada’s Housing Sector Calls for 100,000 New Affordable Homes. CHRA, Feb 4, 2016. http://chra-achru.ca/news/canadas-housing-sector-calls-for-100000-new-affordable-homes

[33] Cost of Homelessness in Canada. Lookout Society, http://lookoutsociety.ca/understanding-homelessness/cost-of-homelessness/the-real-cost-of-homelessness-in-canada

[34] Citizens for Public Justice. www.cpj.ca/infographic-affordable-housing-canada

[35] Housing on First Nations Reserves: Challenges and Successes. Interim Report of the Standing Senate Committee on Aboriginal Peoples, 2015. www.parl.gc.ca/Content/SEN/Committee/412/appa/rep/rep08feb15b-e.pdf

[36] Getting Serious About Affordable Housing: Towards A Plan For Metro Vancouver. Marc Lee, May 2016. CCPA. www.policyalternatives.ca/sites/default/files/uploads/publications/BC%20Office/2016/05/CCPA-BC-Affordable-Housing.pdf

[37] Jobs Created in the U.S. When a Home is Built. NAHB, May 2, 2014. http://eyeonhousing.org/2014/05/jobs-created-in-the-u-s-when-a-home-is-built

[38] 2016 Budget Initiatives for Housing and Real Estate: www.rebgv.org/2016-federal-budget-initiatives-housing-and-real-estate

[39] BC Election 2017. Political Parties Make Promises for Affordable Housing. Vancouver Sun. http://vancouversun.com/news/local-news/the-province-housing-promises

[40] Sweden’s Cooperative Housing: www.housinginternational.coop/co-ops/sweden

[41] Batir son Quartier: www.batirsonquartier.com

[42] How housing co-operatives built a city. Ludwig Franzen, Medium, Oct 7, 2016. https://medium.com/@ludvigfranzn/how-housing-co-operatives-built-a-city-311d2f0c6597#.2ro16j1yq

[43] Community scheme offers blueprint for way out of London’s housing crisis. Positive News, June 28, 2016. www.positive.news/2016/society/21625/community-scheme-offers-blueprint-way-londons-housing-crisis

[44] The Affordable-Housing Crisis Moves Inland. Bloomberg, April 15, 2016. www.bloomberg.com/news/articles/2016-04-15/the-affordable-housing-crisis-moves-inland

[45] Alternative Sources of Capital for the Social/Affordable Housing Sector in Canada. Housing Services Corporation, April 2015. http://share.hscorp.ca/wp-content/uploads/2015/06/Alternative-Sources-of-Capital_Final-for-April-23-FINAL-REPORT-April-17-2015.pdf

[46] WSJ Reports: BND Outperforms Wall Street. Public Banking Institute, Nov 20, 2014. www.publicbankinginstitute.org/bnd_outperforms_wall_street

[47] Murray proposes to expand levy to support affordable housing. Office of the Mayor, Seattle. http://murray.seattle.gov/murray-proposes-to-expand-levy-to-support-affordable-housing/

Nine Reasons To Support A Housing Levy In A Hot Housing Market. Seattle shows: it works, it’s fair, and we need it more than ever before. Sightline, March 21, 2016. www.sightline.org/2016/03/21/nine-reasons-to-support-a-housing-levy-in-a-hot-housing-market/

[48] A better way to tax vacant Vancouver homes. Joshua Gottleib, Globe & Mail, July 25, 2016. www.theglobeandmail.com/opinion/a-better-way-to-tax-vacant-vancouver-homes/article31091843

[49] 10,800 homes remain empty in Vancouver: City Hall. Vancity Buzz, March 8, 2016. www.vancitybuzz.com/2016/03/vancouver-empty-homes-report

[50] UBC economists propose fund to combat housing unaffordability in B.C. UBC News, Jan 18, 2016. http://news.ubc.ca/2016/01/18/ubc-economists-propose-fund-to-combat-housing-unaffordability-in-b-c

[51] City of Vancouver approves empty homes tax. CBC, Nov 16, 2016. www.cbc.ca/news/canada/british-columbia/city-of-vancouver-approves-empty-homes-tax-1.3853542

[52] Real estate loophole lets wealthy buyers save millions in taxes. CTV News, April 16, 2016. http://bc.ctvnews.ca/real-estate-loophole-lets-wealthy-buyers-save-millions-in-taxes-1.2874603

[53] QE for People: www.qe4people.eu

[54] Vancouver’s Housing and Homelessness Strategy 2012-2021: A Home for Everyone http://vancouver.ca/files/cov/Housing-and-Homeless-Strategy-2012-2021pdf.pdf

Vancouver Affordable Housing Agency. http://vancouver.ca/your-government/vancouver-affordable-housing-agency.aspx

[55] For one example, see the Community Housing Land Trust Foundation. www.chf.bc.ca/partner/the-land-trusts

[56] Vancouver Land Trust partnership to create 358 units of affordable housing on City-owned sites. Mayor’s Office, May 25, 2016. http://mayorofvancouver.ca/news/vancouver-land-trust-partnership-create-358-units-affordable-housing-city-owned-sites

On Land Trusts, see also: Housing without debt: Our flawed housing economy, and what we can do about it. Alastair Parvin, Medium, Feb 16, 2016. https://medium.com/@AlastairParvin/housing-without-debt-5ae430b5606a#.wuxchifeb

[57] In 2015, Medicine Hat will become Canada’s first community to end homelessness. Homeless Hub, May 15, 2015. www.homelesshub.ca/blog/2015-medicine-hat-will-become-canadas-first-community-end-homelessness

Canada Could End Homelessness. And It’ll Only Cost You $46 A Year. Huffington Post, Aug 13, 2015. www.huffingtonpost.ca/2015/08/13/housing-first-federal-election_n_7949510.html

[58] 20,000 Homes Campaign. www.20khomes.ca

[59] Designing Flexible Housing. CMHC. www.cmhc-schl.gc.ca/en/inpr/afhoce/afhoce/afhostcast/afhoid/cohode/deflho/deflho_005.cfm

[60] Inside Almere: the Dutch city that’s pioneering alternative housing. The Guardian, Dec 15, 2015. www.theguardian.com/housing-network/2015/dec/15/almere-dutch-city-alternative-housing-custom-build

What Canada could learn from a Dutch self-build housing movement. MacLean’s, Aug 10, 2016. www.macleans.ca/news/world/canada-learn-netherlands-self-build-movement/

[61] Is One of These the Answer to Vancouver’s Affordable Housing Woes? David Ball, The Tyee, March 28, 2016. http://thetyee.ca/News/2016/03/28/Answers-Vancouver-Affordable-Housing-Woes/

[62] Mayor, Council Give Green Light to Pursue Affordable Home Ownership Pilot. Mayor’s Office, April 20, 2016. http://mayorofvancouver.ca/news/mayor-council-give-green-light-pursue-affordable-home-ownership-pilot

[63] City of Vancouver advances toward goal of spurring development of zero-emission green buildings. Georgia Strait, Dec 9, 2015. www.straight.com/news/593461/city-vancouver-advances-toward-goal-spurring-development-zero-emission-green-buildings

[64] House Beautiful: Passive House cuts heating, cooling energy by 90 per cent. Times Colonist, Feb 27, 2016. www.timescolonist.com/life/house-beautiful-passive-house-cuts-heating-cooling-energy-by-90-per-cent-1.2184696

Bernhardt Contracting: http://bernhardtcontracting.com/passive-house/

[65] If it’s Tuesday, this must be a Belgian Passive House tour. Treehugger, March 23, 2015. www.treehugger.com/green-architecture/if-its-tuesday-must-be-belgian-passive-house-tour.html

[66] UBC Student Family Housing http://vancouver.housing.ubc.ca/residences/acadia-park/

[67] Ross Chapin. http://rosschapin.com

[68] Canadian Cohousing Network. http://cohousing.ca

[69] Advocacy, leadership, courage: What we learned from Super InTent City. Maytree, Sept 15, 2016. http://maytree.com/blog/2016/09/advocacy-leadership-courage-what-we-learned-from-super-intent-city/

Guy, in your suggested remedies to the housing crisis you don’t mention how if governments shifted their source of revenue to a land value tax, ignoring the buildings, and shifting taxation off of jobs, business and sales, the market would provide as much affordable housing as needed without government involvement.

LikeLike

Hi Frank, That’s because I’m not persuaded. I believe that good zoning laws and urban containment boundaries do a better job than a simple land value tax would; I worry that it would increase pressure on the land for development, to pay the tax. Can you point me to any working examples, where it is happening, and bringing good results?

LikeLike

Hi there, I wanted to share this to Facebook but it would not allow me… very informational.

LikeLike